yahoo Press

Warner Bros./Paramount Skydance deal spawns $15B leveraged loan, largest since Global Financial Crisis

Images

1 / 5

2 / 5

3 / 5

4 / 5

5 / 5

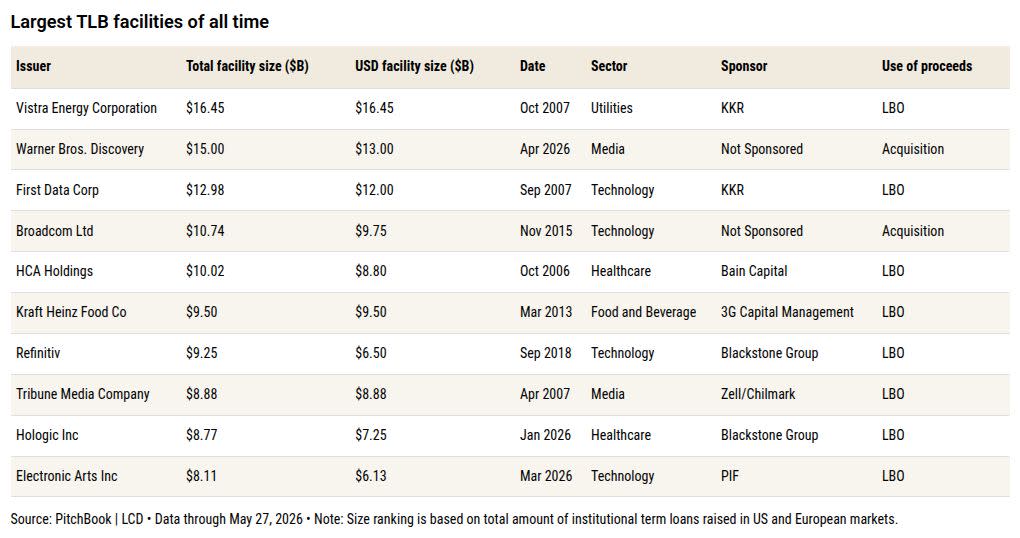

The above button links to Coinbase. Yahoo Finance is not a broker-dealer or investment adviser and does not offer securities or cryptocurrencies for sale or facilitate trading. Coinbase pays us for certain activity generated through this link. Prices displayed are informational. Warner Bros. Discovery (WBD) this week wrapped its $15 billion-equivalent cross-border term loan B financing, a record-setting deal for transaction size in the leveraged loan market. WBD goes into the record books as the second-largest TLB syndication of all time, trailing only the $16.45 billion TXU deal in 2007. For additional context, there have only been three USD institutional loan deals ever totaling $10 billion or more, and two of those were before the Global Financial Crisis. That makes WBD the largest TLB transaction post-GFC, both by the $15 billion total facility size and by the $13 billion US dollar tranche size, topping Broadcom’s November 2015 deal at $10.74 billion across US and European facilities ($9.75 billion in USD). It is also the largest loan ever issued by a non-sponsored borrower. Final tranche sizes for WBD were $13 billion for the US dollar-denominated TLB and €1.717 billion for the euro loan. Final pricing for the seven-year term loans came tight to talk for both spread and OID at S/E+250 with a 99.75 OID. Guidance at launch was S/E+275-300 at 99. Proceeds will be used to refinance a bridge loan the company obtained last year, ahead of the closing of its acquisition by Paramount Skydance Corp. Emergence of the deal came amid a dry season for new M&A supply and is thus contorting volume figures by its sheer size. Consider that the total institutional loan supply in the US from LBO and M&A transactions in May was $17.7 billion (as of May 27), roughly in line with March, with WBD accounting for 73%. Corporate M&A volume jumped to $15.1 billion in May, more than the combined total of January-April, and marking the highest monthly figure since January 2020. Not only did this deal from a debut issuer offer fresh supply to a starved market — indeed, it was upsized from the $5 billion and €1 billion tranche sizes at the initial launch — it came as investors are leaning into higher-quality borrowers. As of May 26, 63% of loans from BB- rated borrowers in the Morningstar LSTA US Leveraged Loan Index were priced at par or higher. That share was at a 2026 high of 76% earlier in May after falling as low as 13% in late March and early April. Despite the dearth of acquisition-related issuance, the market has staged a comeback, led by higher-quality names, from a challenging period earlier this year. For B+ and B issuers, current shares of loans priced at par and above are 48% and 40%, both up from single digits in early March, while B- borrowers lag at 16% (up from 2% on March 2). Companies have taken advantage of the conditions via a wave of refinancing and repricing deals in recent weeks. Speculative-grade borrowers have repriced $50.5 billion of term loans in May, up from just $11.8 billion in February through April combined, with companies rated BB- accounting for 51% of that volume. Sign up for The Credit Pitch Weekly coverage of US and European loans, bonds, private credit, and more. Subscribe Featured image by Pla2na/Getty Images This article originally appeared on PitchBook News Featured image by Pla2na/Getty Images

Comments

You must be logged in to comment.